Info Center

Press Releases

![]() Share

Share

-

Facebook

Facebook

-

LinkedIn

LinkedIn

-

WhatsApp

WhatsApp

-

Email

Email

-

Copy Address

URL copied!

Copy Address

URL copied! -

Print This Page

Print This Page

MPFA blog - Steady growth in MPF reserves

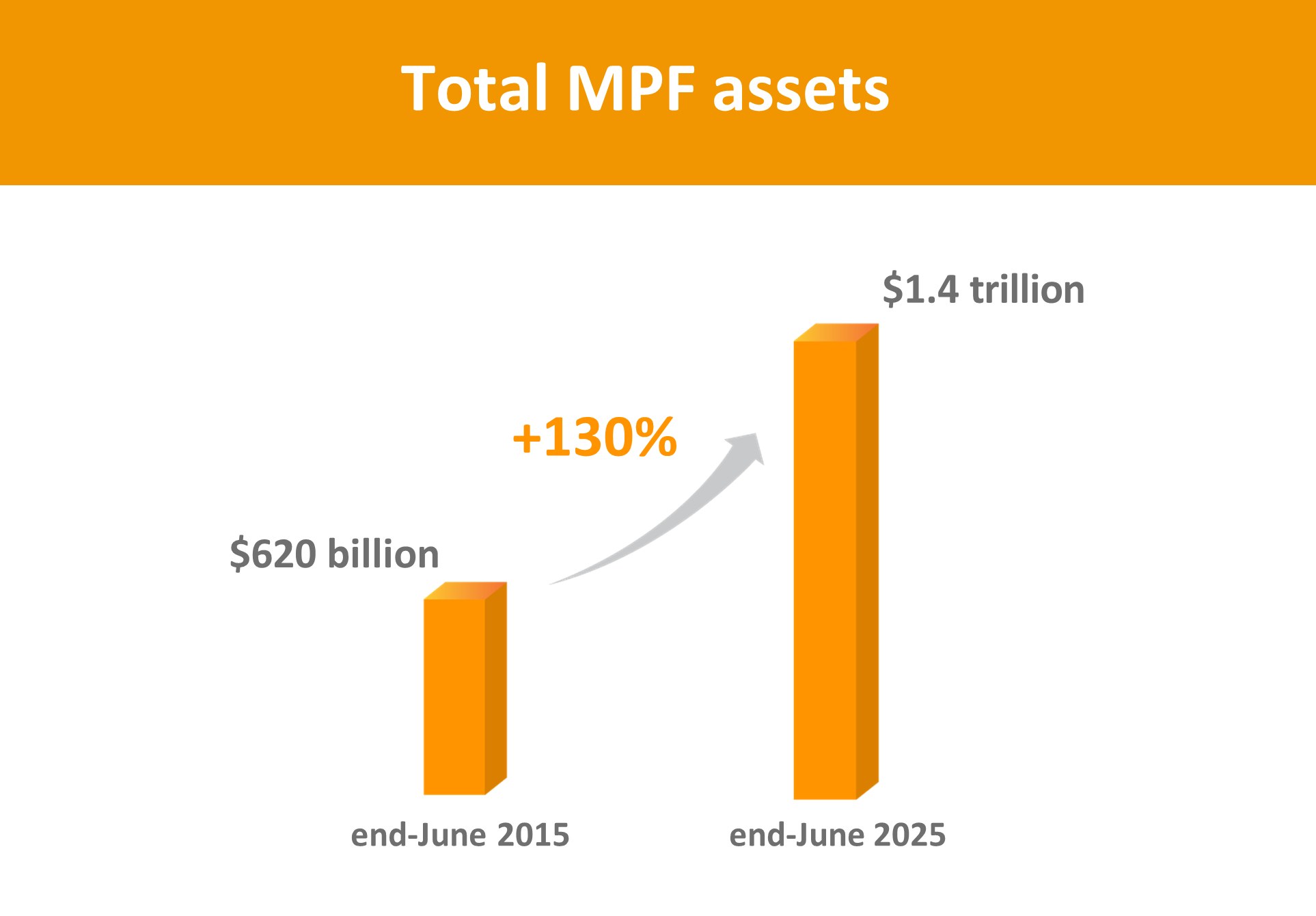

MPFA Chairman Mrs Ayesha Macpherson Lau published a blog post today (27 July), highlighting that since the MPF was implemented over 24 years ago, total MPF assets have again reached a record high, surpassing $1.4 trillion as of end-June 2025, representing an increase of 130% in the past 10 years.

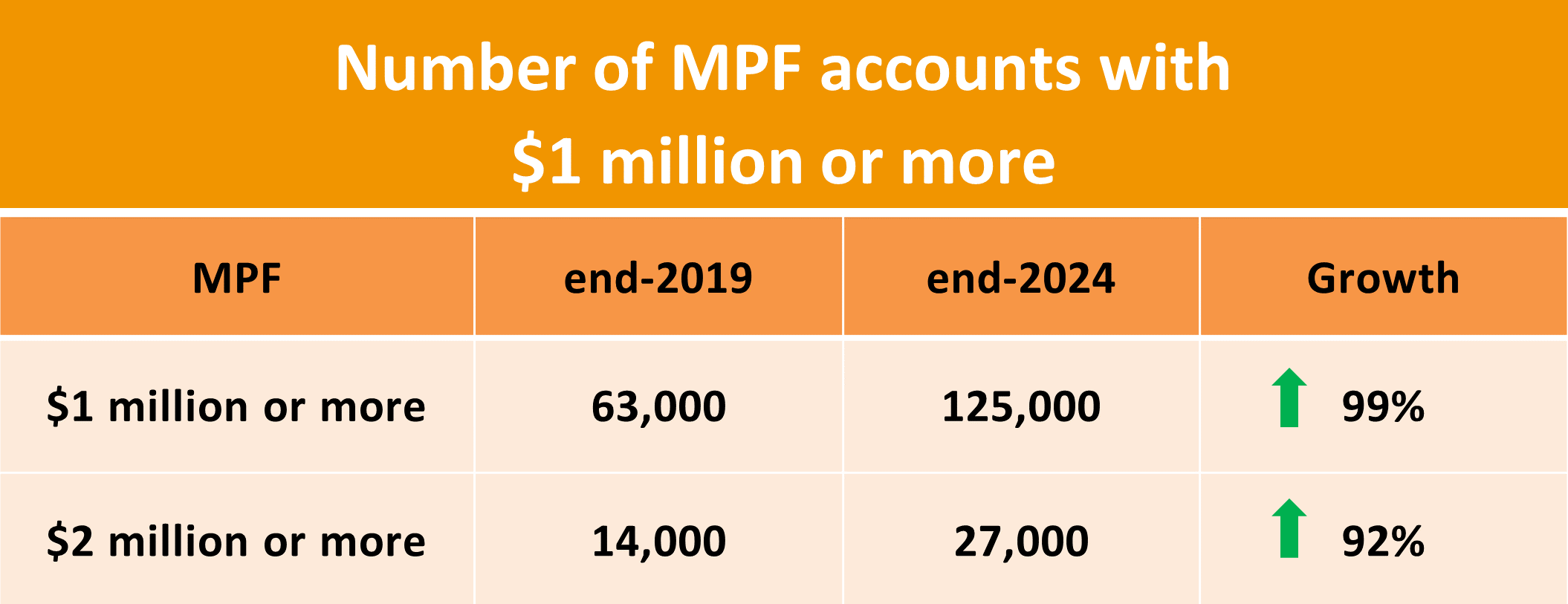

As of end-2024, there were 125,000 MPF accounts with $1 million or more, doubling from 63,000 five years ago, demonstrating the long-term accumulation and compounding potential of the MPF System. Among them:

- 27,000 MPF accounts have accumulated $2 million or more, nearly double the number five years ago; and

- Of the MPF accounts with $1 million or more, 90% (113,000 accounts) were held by scheme members aged 40 or above, while 10% (12,000) were held by those under 40.

Mrs Lau pointed out that the MPF amount scheme members can accumulate depends on various factors. An analysis of a set of accounts with continuous contributions since the inception of the MPF System in December 2000 clearly shows that regular and long-term mandatory contributions by both employers and employees, along with voluntary contributions, play a crucial role in asset accumulation. Among these “senior” accounts, the average MPF accumulated through mandatory contributions is $500,000. 30% of these accounts also include voluntary contributions, averaging $520,000 per account.

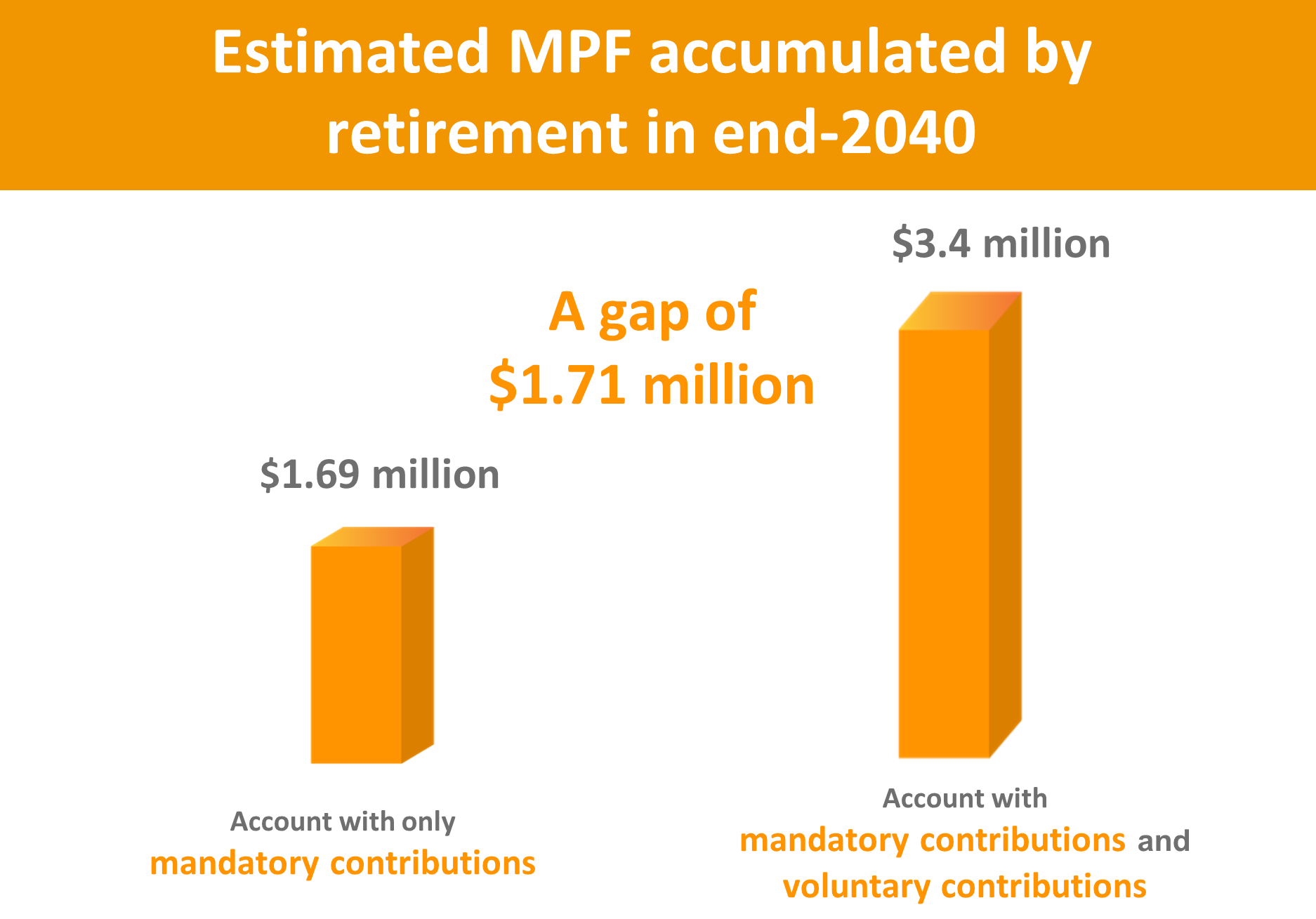

She used the following scenarios to illustrate the importance of compound growth in MPF accumulation over time and the significant impact of voluntary contributions.

Assuming two scheme members who started contributing in 2000 and plan to retire in end-2040, with a 40-year accumulation period:

- Scenario 1: The scheme member made only mandatory MPF contributions; as of end-2024, the account balance was $500,000 with reference to the data presented above.

- Scenario 2: The scheme member made both mandatory and voluntary contributions. As of end-2024, the account balance was $1.02 million, $520,000 of which was from voluntary contributions.

Both earn the current median monthly income of $20,500, with salary growth projected in line with long-term trends. It is assumed that going forward the two scheme members will invest their MPF in the default investment strategy (DIS), commonly called “funds for lazy people”, which automatically adjusts the mix between higher- and lower-risk assets from age 50 onwards to mitigate investment risk. The following projections are made based on the performance of the funds under DIS since its launch, namely the Core Accumulation Fund (annualized net return rate of 6.5%) and Age 65 Plus Fund (annualized net return rate of 2.4%):

- Scenario 1: If only mandatory contributions are made going forward, the estimated total MPF accumulated upon retirement in end-2040 is $1.69 million.

- Scenario 2: With both mandatory contributions and additional voluntary contributions at 10% of relevant income, the projected total will reach $3.4 million in end-2040, which is $1.71 million higher than that in Scenario 1.

She further emphasized that it is never too late for scheme members to start making voluntary contributions, even at the mid-career stage. Using Scenario 1 as an example, although that scheme member had made only mandatory contributions previously, starting to make voluntary contributions at 10% of the relevant income from this year onwards is projected to have a total balance of $2.36 million by retirement in end-2040, an increase of $670,000 compared to continuing with mandatory contributions alone.

The above projection is only for illustrative purposes. The actual accumulation will depend on the scheme member’s contribution amount and investment choice. However, it clearly demonstrates that making additional voluntary contributions on top of mandatory contributions plays a crucial role in boosting the growth of one’s accrued MPF benefits.

She also reminded scheme members that the MPF is a long-term investment. With early planning and leveraging voluntary contributions, individuals can steadily build reliable financial reserves through the MPF for their basic retirement protection.

For the full version of the article, please visit the MPFA blog. The blog is available in Chinese only.

– Ends –

27 July 2025