Enforcement

Enforcement Alerts

![]() Share

Share

-

Facebook

Facebook

-

LinkedIn

LinkedIn

-

WhatsApp

WhatsApp

-

Email

Email

-

Copy Address

URL copied!

Copy Address

URL copied! -

Print This Page

Print This Page

MPF Enrolment and Contributions - Smart Tips

It is employers’ legal obligation under the MPF System to enrol new employees into the MPF scheme that the employers are participating. Except for exempt persons, employers should enrol both full-time and part-time employees who are at least 18 but under 65 years of age in an MPF scheme within the first 60 days of employment. The 60-day employment rule does not apply to casual employees in the construction and catering industries. (Please refer to the link “Enrolling Employees”)

When handling MPF contributions, employers should be mindful of the misconceptions listed in the link below to avoid employers’ payment being considered late or default. (Please refer to the document “Common Misconceptions in Handling MPF Contributions”

The MPFA takes enforcement actions against non-compliant employers who are found to have failed to make payment of MPF contributions timely, deducted employer’s contributions from an employee's pay, or failed to enrol their employees in an MPF scheme. These enforcement measures may include:

- Requesting employers to rectify the situation immediately

- Imposing a contribution surcharge of 5% on defaulting employers

- Filing a civil claim in court to recover mandatory contributions and surcharges in arrears

- Imposing financial penalties on non-compliant employers

- Prosecuting non-compliant employers or persons, including their officers, directors and partners

Employees may take the following steps to protect their MPF’s rights:

- Confirm that the employer had enrolled the employee into an MPF scheme.

The employee would receive documents/notifications from eMPF Platform upon enrollment into an MPF scheme. You may learn more about the “MPF Documents Received by Scheme Members under Different Stages” on our website.

- Regularly check the MPF contribution records on the eMPF Platform to confirm the employer has made contributions on time.

Under the law, the employer is required to provide an employee with a monthly MPF contribution record. You may learn more about the “Monthly Contribution Record” on our website.

If an employee suspects that his/her employer has failed to make contributions, he/she should first clarify with the employer or the trustee to avoid any misunderstanding. If the employer has indeed defaulted on contributions, the employee should contact MPFA immediately to lodge a complaint.

MPFA will investigate complaints and proactively inspect employers’ premises, and will take enforcement measures against non-compliant employers (including those who are found to have evaded payment of MPF contributions, deducted employer’s contributions from an employee's pay, or failed to enrol employees in an MPF scheme). You may learn more about the “Enforcement Measures and Penalties against Non-compliant Employers” on our website.

Apart from exempt persons, all SEPs aged 18 to 64 must enrol themselves into an MPF scheme within the first 60 days of being self-employed. SEPs are required to make contributions at a regular interval (the contribution amount is 5% of their relevant income and it is subject to the minimum and maximum relevant income levels). In addition, SEPs can opt to make mandatory contributions on a monthly or yearly basis.

If an SEP fails to enrol in an MPF scheme or pay contribution on time, the SEP is liable to a maximum fine of $50,000 and imprisonment for six months.

You may learn more about the “enrolment for Self-employed persons” and the determination of “relevant income” on our website.

Cessation of self-employment

If an SEP ceases to be self-employed (such as being employed by an employer), he/she must, update his/her termination date on the eMPF Platform on or before the next contribution day and pay the last contribution before the last day of the contribution period.

If an SEP fails to report the date of cessation of self-employment, the SEP may be liable to a financial penalty (from $5,000 to $20,000 subject to any previous failure).

Alerts and Tips on Scams

Defrauding Tricks

The MPFA has recently received enquiries from scheme members who had received phone calls from persons claiming to be calling from the MPFA or eMPF Platform Company, inviting them for a meeting to introduce MPF products or documents and requesting them to provide their personal information.

Anti-fraud Tips

- The MPFA and eMPF Platform Company never contact individual scheme members by phone to introduce MPF products/documents or request scheme members to provide their personal information or details of their MPF accounts over the phone;

- If scheme members receive a suspicious call or other forms of communication from someone claiming to be representative of the MPFA or eMPF Platform Company, call the MPFA hotline 2918 0102 or eMPF Customer Service hotline 183 2622 to verify the identity of the caller or the authenticity of the message;

- Do not disclose any personal information to strangers;

- Remind your family and friends to stay alert against deception;

- If you suspect that you have fallen prey to fraud, please approach the Police immediately for assistance.

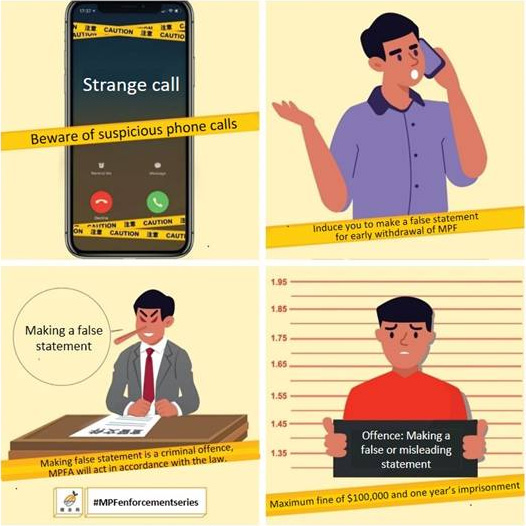

MPFA reminds MPF scheme members to be vigilant against unsolicited calls, text messages or social media posts from suspected crime syndicates that offer to help them make early withdrawal of MPF.

Some common features or malpractices perpetrated by the crime syndicates include:

- the person who contacts the scheme member is not a registered MPF intermediary. In some cases, the person might falsely claim to be a registered intermediary attached to a principal intermediary (PI) and offers to help the scheme member apply for early withdrawal of MPF;

- advising the scheme member to make a false statutory declaration in order to withdraw their MPF on the ground of permanent departure from Hong Kong;

- advising or assisting the scheme member to apply for withdrawal of MPF by submitting false supporting documents to the MPF trustee;

- charging a high percentage of the amount of MPF withdrawn by the scheme member as commission or handling fees; and

- persuading the scheme member to invest the withdrawn MPF into some suspicious overseas investment plan.

MPFA reminds scheme members not to fall prey to crime syndicates and risk breaching the law. Making a false declaration is a serious criminal offence that is punishable by imprisonment and fine. (Please refer to the press release "Jail sentence for false claim for MPF withdrawal").

To protect their interests, scheme members should:

- not disclose any personal information to any unknown third parties;

- if the identity of the intermediary is in doubt, check the MPFA’s register1 and contact the PI concerned to confirm the identity of the alleged intermediary;

- not sign on any blank or incomplete forms;

- obtain and keep a copy of all signed documents; and

- report any suspicious fraudulent activity to MPFA or the Police.

MPFA has reminded MPF trustees to stay vigilant in assessing claims for MPF withdrawal in order to detect possible false claims. MPFA will continue to work closely with the Police and frontline regulators (namely, Hong Kong Monetary Authority, Insurance Authority and Securities and Futures Commission) to combat such crimes and malpractices.

Last but not least, scheme members might risk losing part or all of their retirement savings by making rash investment decisions under the influence of crime syndicates on illegitimate or unregulated investment products. MPF is a long-term savings scheme for retirement. Withdrawing MPF early will have an impact on the scheme member's retirement savings.

Following the ongoing supervisory initiatives by the MPFA, all MPF intermediaries have ceased conducting unsolicited calls (commonly known as cold calls) for marketing MPF-related products or services since February 2025 in response to growing concern over potential scam calls purportedly related to MPF. On 31 March 2025, the MPFA issued a circular letter reminding all MPF intermediaries not to conduct any unsolicited telemarketing activities in respect of MPF-related products or services.

However, MPF intermediaries may still contact MPF scheme members by phone to follow up on MPF-related matters to provide services such as assisting with opening accounts or switching schemes.

Anti-fraud Tips

If members of the public receive cold calls from unknown individuals claiming to be intermediaries selling MPF, they should hang up immediately to protect themselves from potential scams. If the caller claims to be following up on MPF-related matters, scheme members should obtain the following information from the caller:

- Full name of the caller;

- If the caller is an subsidiary intermediary1, the MPF registration number of the caller;

- Name of the MPF intermediary companies (principal intermediaries2); and

- Purpose of the call.

and then verify the caller’s identity with the relevant MPF intermediary company to protect themselves. Information and designated phone numbers of MPF intermediary companies3 can be found on the MPFA website.

Furthermore, to protect their interests, scheme members should:

- not disclose any personal information to any unknown third parties;

- not sign on any blank or incomplete forms;

- obtain and keep copy of signed forms;

- if the identity of the intermediary is in doubt, check the MPFA’s register and contact the principal intermediary concerned to confirm the identity of the alleged intermediary; and

- report any suspicious fraudulent activity to the Police.

Reporting Suspicious Activities

If you suspect that you have been targeted by scam calls or fraudulent activities impersonating MPF intermediaries, please report the matter to the Police immediately. You may also contact the MPFA hotline at 2918 0102 or Police for enquiries or visit Police's Anti-Deception Coordination Centre's website (www.adcc.gov.hk).

Protect Yourself Against Scams

The MPFA, together with the Police and other financial regulators, continues to strengthen measures to combat fraud and protect scheme members. Your vigilance and prompt reporting can help prevent scams and protect the community.

- A subsidiary intermediary is a person registered by the MPFA to carry out MPF sales and marketing activities and to give regulated advice on behalf of a principal intermediary to which the person is attached.

- A principal intermediary is a business entity registered by the MPFA to engage in conducting MPF sales and marketing activities and giving regulated advice.

- List of the designated telephone numbers of 20 principal intermediaries with the highest numbers of subsidiary intermediaries.

|

Name:

|

International Private Banking Hong Kong

|

|

Website:

|

https://interprivatesbankinghk.com/

|

|

Alert Date: |

15 January 2026

|

|

Remarks: |

According to MPFA records, this entity is not a recipient of the Good MPF Employer Award. Details about the Good MPF Employer Award can be found on the MPFA website (Good MPF Employer Award).

A list of authorized institutions supervised by the Hong Kong Monetary Authority (HKMA) is available on the HKMA website (www.hkma.gov.hk) for public inquiry.

|

|

Name:

|

Shao Bank

|

|

Website:

|

www.shaobank.com

|

|

Alert Date: |

8 June 2023

|

|

Remarks: |

This entity falsely claims on its website that it has a relationship with the MPFA. The MPFA does not have any relationship with this entity. Public registers of entities approved by or registered with the MPFA can be found on the MPFA website (www.mpfa.org.hk). |

(The following YouTube video and MPFA Facebook page are available only in Chinese version)

YouTube Video

Don’t fall prey to crime syndicates’ claims that such withdrawals are legal!

Making false claims for MPF on grounds of permanent departure from Hong Kong is a criminal offence!

Facebook Video

Facebook Post

Stay tuned to the MPFA’s LinkedIn page for more tips on how to avoid falling prey to scam calls.

(LinkedIn posts are available only in English version)

Improper Acts of MPF Intermediaries

Scheme members should stay alert to the following possible improper conduct and practices by non-compliant MPF intermediaries*:

- misuse a scheme member’s personal information obtained at meetings to carry out transfers of MPF without the member’s authorization;

- fail to explain clearly to a scheme member the contents and purposes of MPF forms that the scheme member has signed during meetings with the intermediary. As a consequence, some transfers not intended or authorized by the scheme member are done;

- conduct fraudulent acts, such as falsifying documents, forging a member’s signature, using the member’s information previously obtained to make another transfer and submit the forms to the trustee without the member’s authorization;

- impersonate a scheme member to call the trustee of an MPF scheme to obtain the member’s account information for the purpose of effecting MPF transfers;

- impersonate the representative of a government agency or public body (e.g. staff of MPFA) when approaching a scheme member;

- provide inaccurate or misleading information about MPF schemes or funds to scheme members;

- allow a scheme member to sign on a blank or incomplete form without clearly explaining the contents and purposes;

- fail to provide copies of the signed forms or documents to a scheme member after signing;

- fail to execute a scheme member’s instruction promptly and accurately or to alert the scheme member to any delay in execution; and

- use or provide a scheme member with marketing materials that have not been approved by the principal intermediary.

* The eMPF Platform has now taken over the administration of MPF schemes. Intermediaries should ensure that all information provided, submissions made and actions taken are accurate and compliant. For more details, please visit eMPF Website (www.empf.org.hk).