MPF System

Mandatory Contributions

![]() Share

Share

-

Facebook

Facebook

-

LinkedIn

LinkedIn

-

WhatsApp

WhatsApp

-

Email

Email

-

Copy Address

URL copied!

Copy Address

URL copied! -

Print This Page

Print This Page

Mandatory contributions made for an employee are fully and immediately vested in the employee once they are paid into his/her MPF account. Any investment return derived from the mandatory contributions is also fully and immediately vested in that employee.

Regular employees

Employees and employers are both required to make mandatory contributions of 5% of the employee’s relevant income into the employee’s MPF account, subject to the minimum and maximum relevant income levels.

Employers must make mandatory contributions for their employees with their own funds. They must also deduct the employee’s contributions from his/her relevant income for each contribution period (generally the wage period).

For monthly paid employees, the current minimum and maximum relevant income levels are $7,100 and $30,000 respectively.

Learn about the adjustments made to the minimum and maximum relevant income levels for employee contributions ![]() over the years.

over the years.

Monthly paid employees

|

Monthly Relevant Income

|

Employer's Mandatory Contribution

|

Employee's Mandatory Contribution

|

|---|---|---|

|

Less than $7,100

|

Relevant income x 5%

|

No contribution is required

|

|

$7,100 to $30,000

|

Relevant income x 5%

|

Relevant income x 5%

|

|

More than $30,000

|

$1,500

|

$1,500

|

Non-monthly paid employees

If an employee is paid daily, weekly or bi-monthly, the employer must first calculate the minimum and maximum relevant income levels of the wage period based on the daily minimum and maximum relevant income levels of $280 and $1,000. The contributions to be made should be determined as follows:

|

Relevant Income of Employee

|

Employer's Mandatory Contribution

|

Employee's Mandatory Contribution

|

|---|---|---|

|

Less than the minimum level ($280 x number of days in the wage period)

|

Relevant income x 5%

|

No contribution is required

|

|

Between the minimum and maximum levels

|

Relevant income x 5%

|

Relevant income x 5%

|

|

More than the maximum level ($1,000 x number of days in the wage period)

|

Maximum level x 5%

|

Maximum level x 5%

|

|

Relevant Income of Employee

|

Employer's Mandatory Contribution

|

Employee's Mandatory Contribution

|

|---|---|---|

|

Less than the minimum level ($1,960)

|

Relevant income x 5%

|

No contribution is required

|

|

Between the minimum and maximum levels ($1,960 to $7,000)

|

Relevant income x 5%

|

Relevant income x 5%

|

|

More than the maximum level ($7,000)

|

Maximum level x 5%

|

Maximum level x 5%

|

Relevant income refers to all monetary payments paid or payable by an employer to an employee.

Including: any wages, salary, leave pay, fees, commissions, bonuses, gratuities, perquisites or allowances

Excluding: severance payments or long service payments under the Employment Ordinance

Examples

The following is a list of examples of different types of income:

|

Types of Income

|

Relevant Income? (Y/N)

|

|---|---|

|

1. Wages and Salaries

|

|

|

13th month pay (double pay)

|

Y (How many months of pay an employee receives is determined by his/her employment contract)

|

|

Bonus

|

Y

|

|

End-of-contract gratuity

|

Y

|

|

2. Reimbursement / Allowance

|

|

|

Nature of reimbursement

|

N (Reimbursement of expenses incurred by employees for employment related goods and services which are necessary in the performance of employment duties)

|

|

Cash allowance

|

Y (Allowance provided by the employer in cash, which employees may spend as they see fit)

|

|

Internship allowance

|

Y (Allowance provided by the employer in cash in connection with a vocational training programme)

|

|

Paid leave allowance

|

Y

|

|

3. Transportation and Car Subsidy

|

|

|

Transportation subsidy

|

N (Non-monetary benefits)

|

|

Car subsidy

|

N (Non-monetary benefits)

|

|

Car subsidy in cash

|

Y (Employer provides cash payment for the benefit of employees)

|

|

4. Commission

|

|

|

Calculated based on transaction amount, number of transactions or on project basis

|

Y |

|

5. Tips

|

|

|

Tips collected by the employer

|

Y (Tips collected via the employer and service charges included in the bill (including the tips given by customers when paying the bill with a credit card) which are subsequently distributed partly or fully to employees)

|

|

Tips not collected by the employer |

N (The tips paid directly to employees, put in a tip box or left on the table by customers. (The tips are retained by the employee or shared among employees without any intervention by the employer.))

|

|

6. Employee Benefits

|

|

|

Marriage gifts |

N

|

|

Holiday tour package

|

N (Non-monetary benefits. Expenses paid by the employer to cover expenses included in the holiday package, such as transportation, accommodation, food, etc.)

|

|

Meals consumed on the spot

|

N (Non-monetary benefits)

|

|

Meals provided in the form of vouchers |

N (Non-monetary benefits)

|

|

7. Court Award and Termination Payment

|

|

|

Award determined by a court or tribunal as:

|

Y

|

|

Payment in lieu of notice

|

N (Payment that does not fall within the definition of relevant income (i.e. not wages, salary, leave pay, fee, commission, bonus, gratuity, perquisite or allowance))

|

|

Severance payment

|

N (Specifically excluded from the definition of “relevant income”)

|

|

Long service payment |

N (Specifically excluded from the definition of “relevant income”)

|

|

8. Others

|

|

|

Dividend income |

N (Returns on investment received by shareholders)

|

|

Share options

|

N (Non-monetary benefits)

|

|

Gains realised from share options

|

N

|

|

Medical claims reimbursement |

N (Payments that are made by third parties, rather than the employer, to employees pursuant to an insurance contract purchased by the employer covering the employees)

|

|

Employment-related medical expenses paid directly by the employer

|

N

|

Monthly paid employees

Generally, for employees who are paid on a monthly basis, the contribution day is the 10th day of each month. For example, contributions for the wage period of September should be paid to the eMPF Platform on or before 10 October.

For new employees, employers must make their first-time contributions to the eMPF Platform on or before the next contribution day (the 10th day of each month) after the calendar month in which the 60th day of employment falls.

If the contribution day falls on a Saturday, a public holiday, a gale/black rainstorm warning day or a day on which the eMPF Platform is suspended (and the suspension affects the performance of the relevant duty of an employer), the contribution day is extended to the next day which is not a Saturday, a public holiday, a gale/black rainstorm warning day or a day on which the eMPF Platform is suspended (and the suspension affects the performance of the relevant duty of an employer).

For the contribution day of each month in this year, please refer to the MPF Contribution Days Calendar. A digital version of the calendar can be installed on Android and iOS devices.

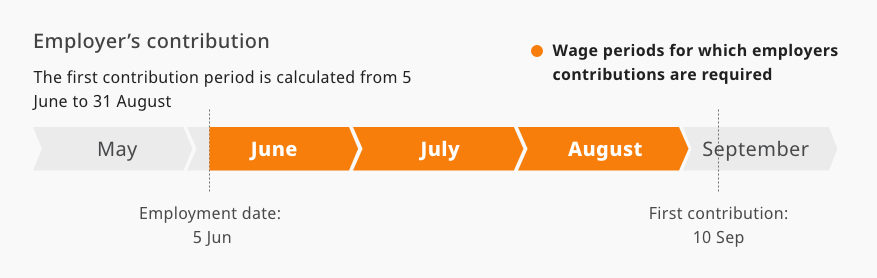

Employer’s contribution period

Generally, the contribution period refers to the wage period. The calculation of an employer’s contribution for an employee should begin from the first day of the employee’s employment.

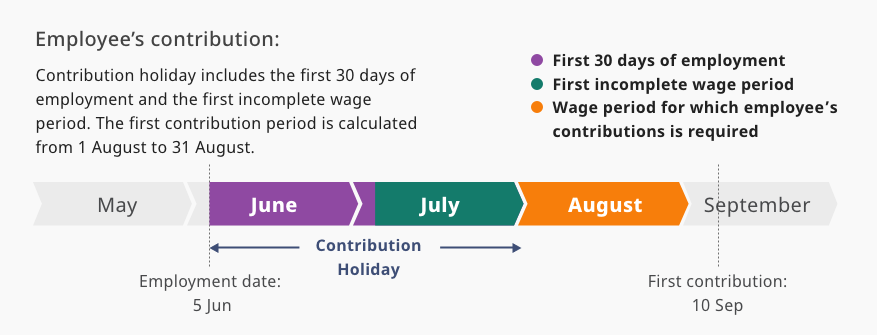

Employee’s contribution period

New employees enjoy a contribution holiday, meaning that they are not required to make contributions for the first 30 days of employment, nor do they have to make contributions for:

- any incomplete wage period that immediately follows the 30-day contribution holiday (if the employee’s wage period is a month or shorter than a month); or

- the calendar month in which the 30th day of employment falls (if the employee’s wage period is longer than a month).

Example

Ms D’s first day of employment is 5 June. Since she enjoys a contribution holiday for the first 30 days of employment, no MPF contribution should be deducted from her income earned during the 30-day period, i.e, from 5 June to 4 July.

In addition, since her 30th day of employment falls in July, she is not required to make MPF contribution for July (because the contribution holiday extends to the end of the incomplete wage period that immediately follows the 30-day period). The employer should only deduct MPF contribution from Ms D’s income for the contribution period of August and remit the contribution to the eMPF Platform on or before 10 September.

Given the contribution holiday does not apply to the employer, the employer’s contributions for Ms D should be calculated from her first day of employment, i.e. 5 June.

When to submit?

Employers must provide the eMPF Platform with a remittance statement when they make contributions to the eMPF Platform.

What if an employee has no relevant income for a particular contribution period?

Even if an employee has no relevant income for a contribution period, the employer is still required to include that employee in the remittance statement. The employer should report '$0' as the employee’s relevant income, or fill in the remittance statement according to the eMPF Platform's instructions.

Monthly pay-record

For every month, after remitting contributions to the eMPF Platform, employers should provide each employee with a monthly pay-record within seven working days. The pay-record should include the following information:

- the employee’s relevant income

- the amount of mandatory contributions made respectively by the employer and the employee

- the amount of voluntary contributions (if any) made respectively by the employer and the employee

- the date on which the contributions were paid to the eMPF Platform

Annual benefit statement

The eMPF Platform will provide scheme members with an annual benefit statement (ABS) within three months after the end of each financial period.

ABS must set out:

- the total amount of contributions the employer paid for the employee during the year;

- the opening and closing balances of the MPF account for the year; and

- the gains and losses associated with the MPF account during the year.

Employees' responsibilities

Employees should regularly check their pay-records and ensure that contributions are made on time by their employers and the amounts are correct.

Employees' rights

Employees may check their account details via the eMPF Platform.

Lodging a complaint

If an employee suspects that his/her employer has failed to make contributions, he/she should first clarify with the employer or the eMPF Platform. If the employer has indeed defaulted on contributions, the employee should contact MPFA immediately to lodge a complaint.

Persons employed in the construction industry and the catering industry for less than 60 days (Casual employees)

If employers choose to enrol their casual employees in a Master Trust Scheme, please note that:

- Their contributions shall be calculated in the same way as those for a regular employee.

- Casual employees do not have a contribution holiday.

- Employers shall pay the contributions within 10 days after each contribution period ends (even if the contribution period is less than one month). If the contribution day falls on a Saturday, a public holiday, a gale/black rainstorm warning day or a day on which the eMPF Platform is suspended (and the suspension affects the performance of the relevant duty of an employer), the contribution day will be extended to the next day which is not a Saturday, a public holiday, a gale/black rainstorm warning day or a day on which the eMPF Platform is suspended (and the suspension affects the performance of the relevant duty of an employer).

- Employers must provide the eMPF Platform with a remittance statement when they make contributions to the eMPF Platform.

- Employers should also provide each employee with a monthly pay-record and keep the contribution record.

If employers choose to enrol their casual employees in an Industry Scheme, the calculation of contributions is different from that for casual employees in a Master Trust Scheme. For details, please refer to Industry Schemes.